They choose not to believe our accountant.

They choose not to believe our accountant and use a fake FAS course to pay for one of their own.

On the 29th of July I called Mr. O’Connor’s manager Mr. Brian Quinlan and appealed to him to take Mr. O’Connor off the case and put someone else in to look at our company.

On the 2nd of August at 9.30am we had a meeting at Forbairt Cork. Present at this meeting were from Forbairt were Mr. Brian Quinlan, Mr. Mort O'Connor, Mr. Kevin Sherry. From Holts were Mr. Russell, Ms. Janssen and Mr. Sheehan.

1996-08-09-for-hol-1.jpg |

1996-08-09-for-hol-2.jpg |

1996-08-20-fas-hol.jpg |

Mr. Sherry was refreshingly businesslike and saw that the problem was that Forbairt did not accept Mr. Sheehan’s figures. He therefore decided that Forbairt would put in an accountant to verify the figures. While Mr. Sheehan found the suggestions with regard to his figures insulting, all in all we felt that it was a constructive meeting.

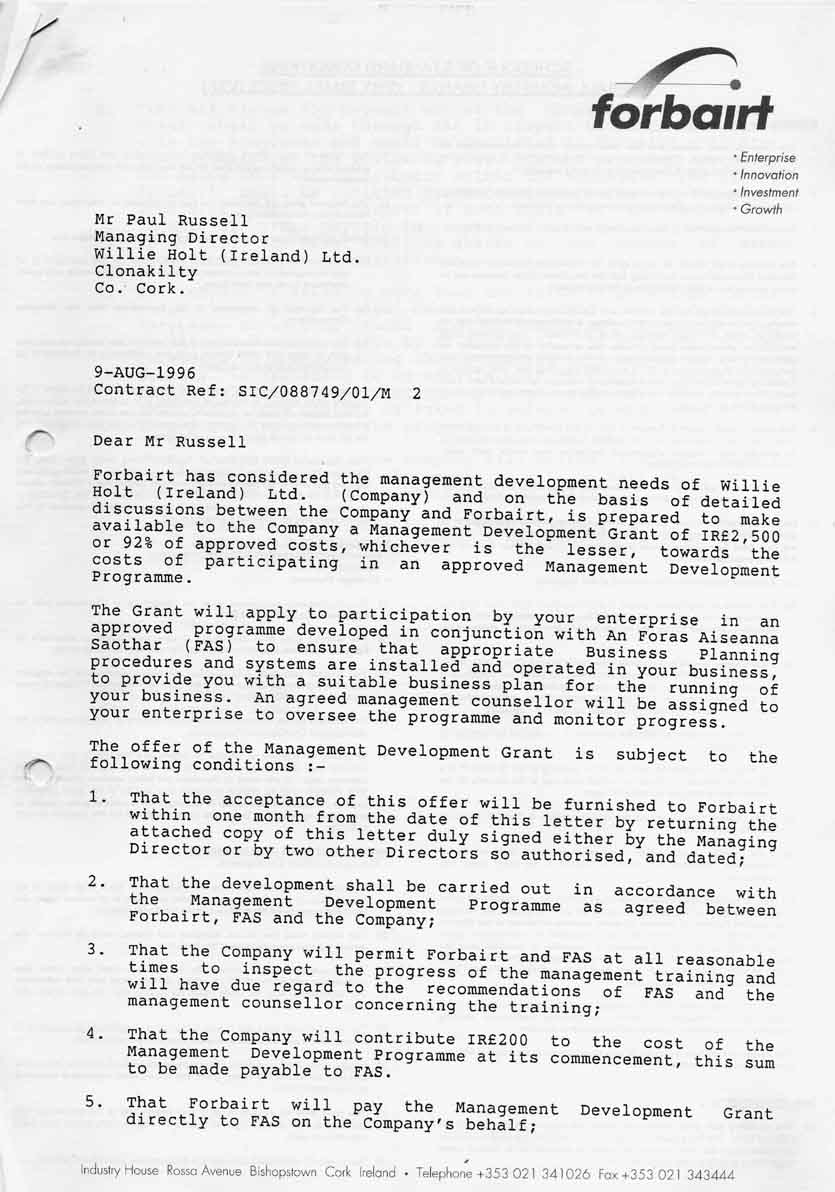

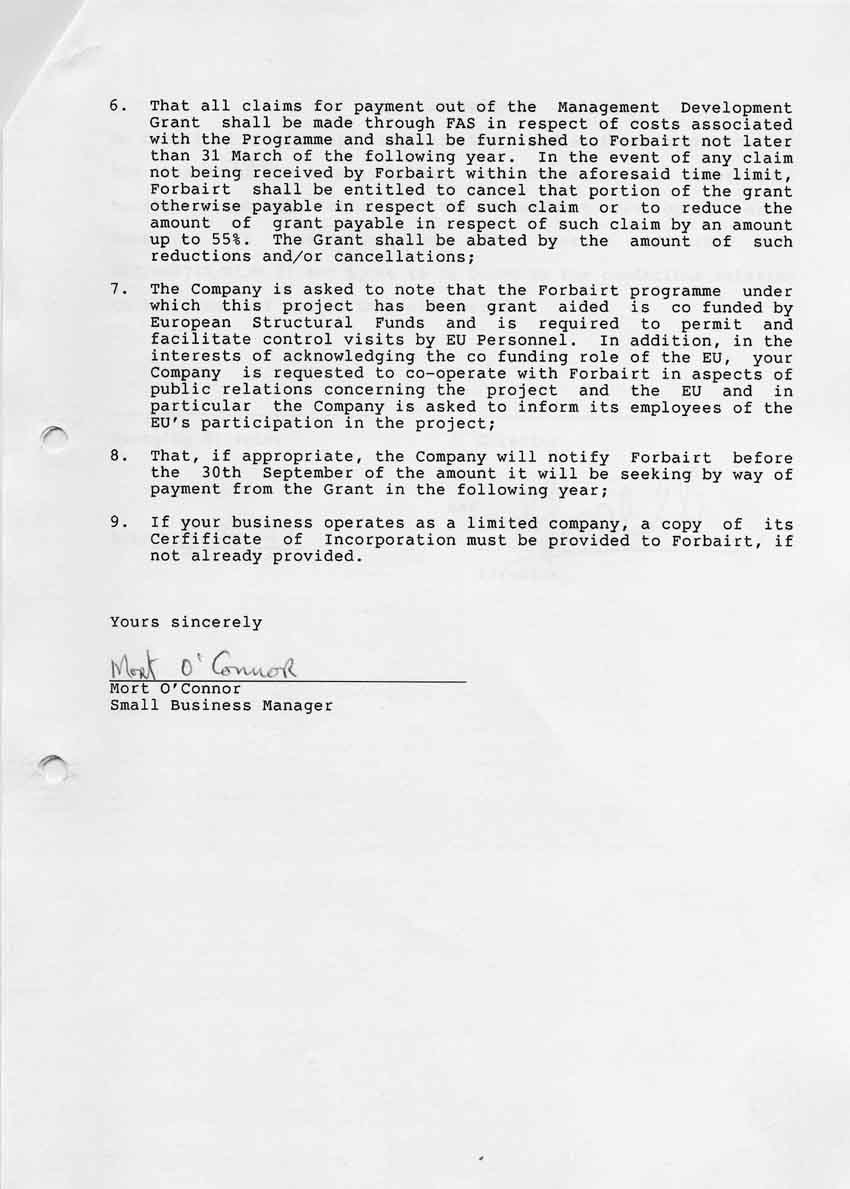

On the 9th of August Mr. O'Connor visits the factory and surprises us by asking us to sign some papers to allow for the appointment of an "independent accountant" to check the accounts for Forbairt. You will note from this document that Forbairt is defrauding EU funds. The accountant is to be paid from EU funds under a "Management Development Grant Contract SIC/088749/01/M 2". This had nothing to do with “Management Development.” It was simply Forbairt spending money because they did not believe Mr. Sheen's figures.

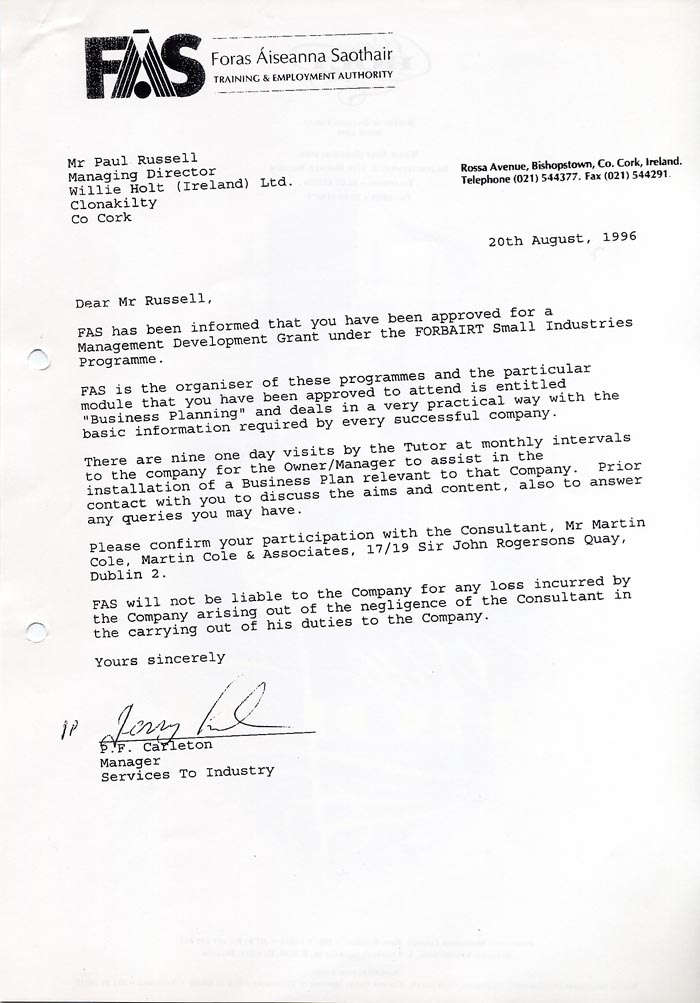

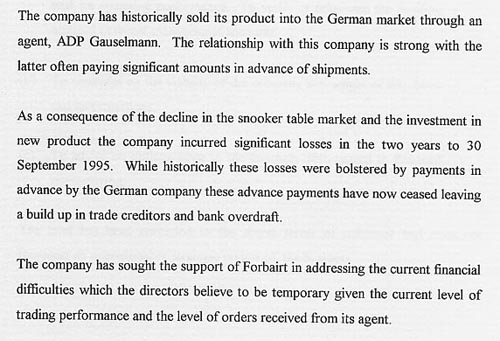

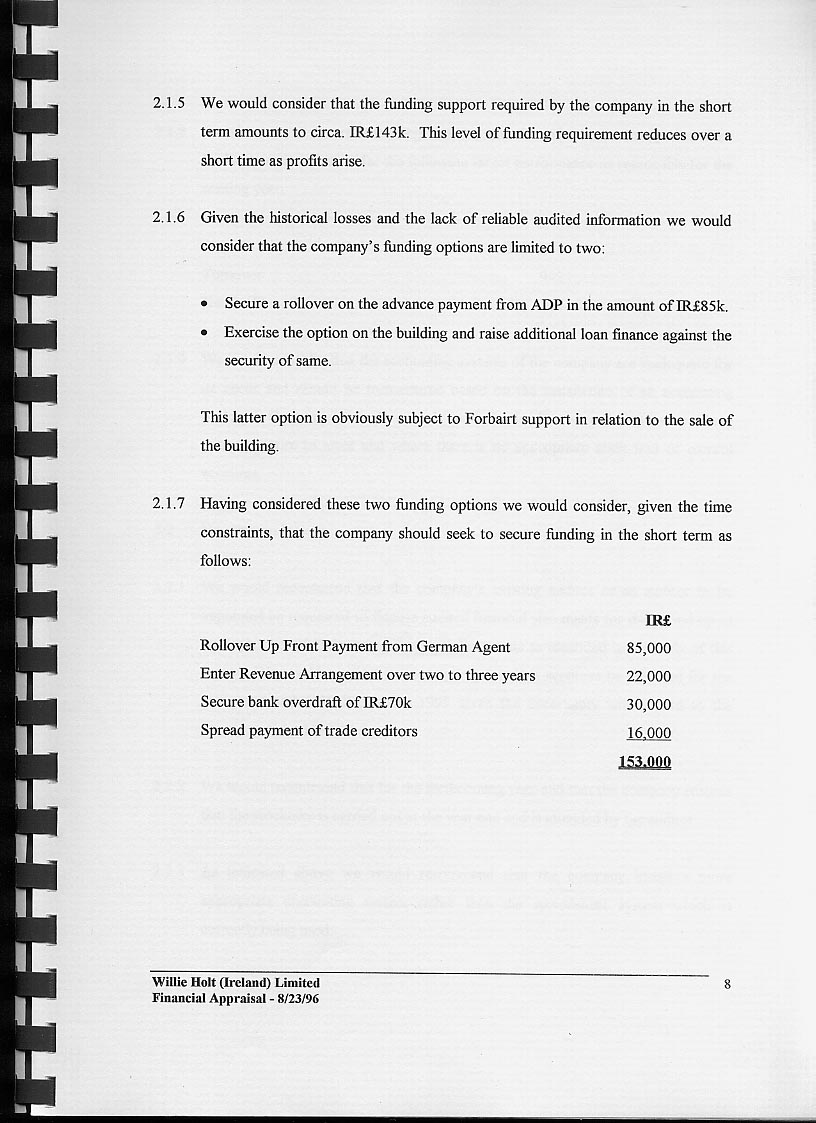

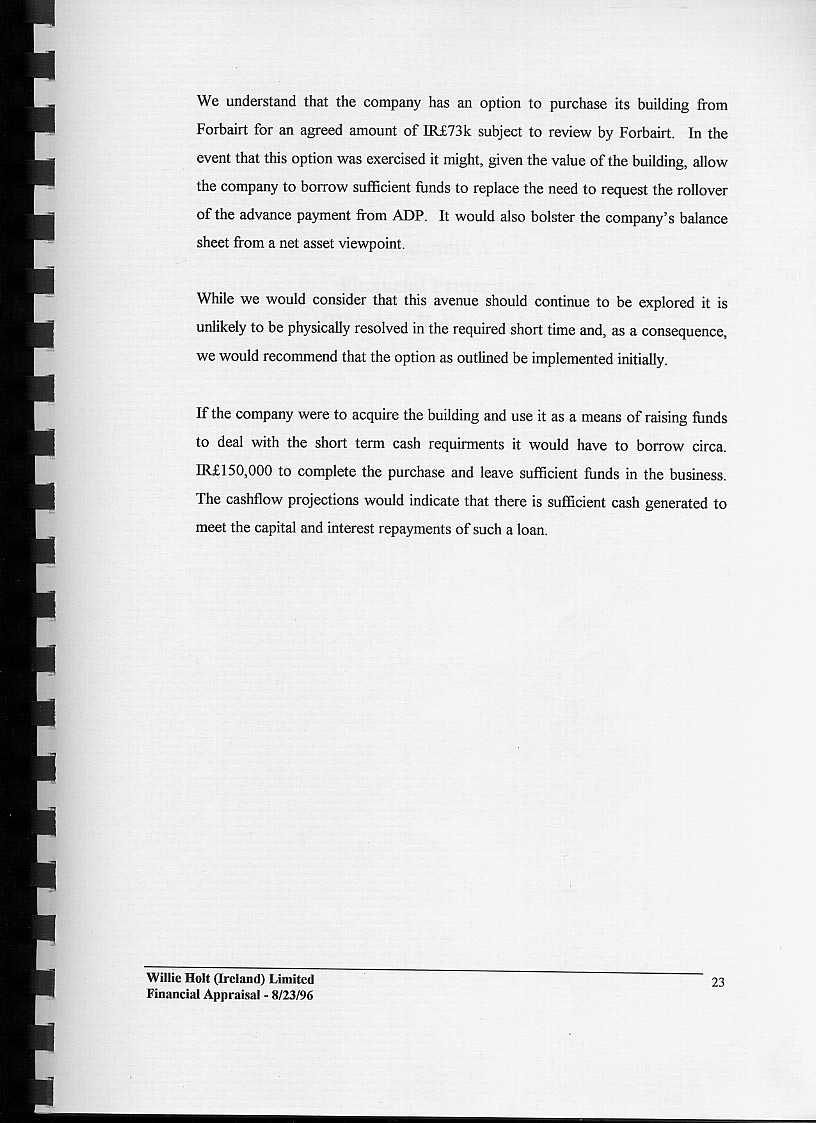

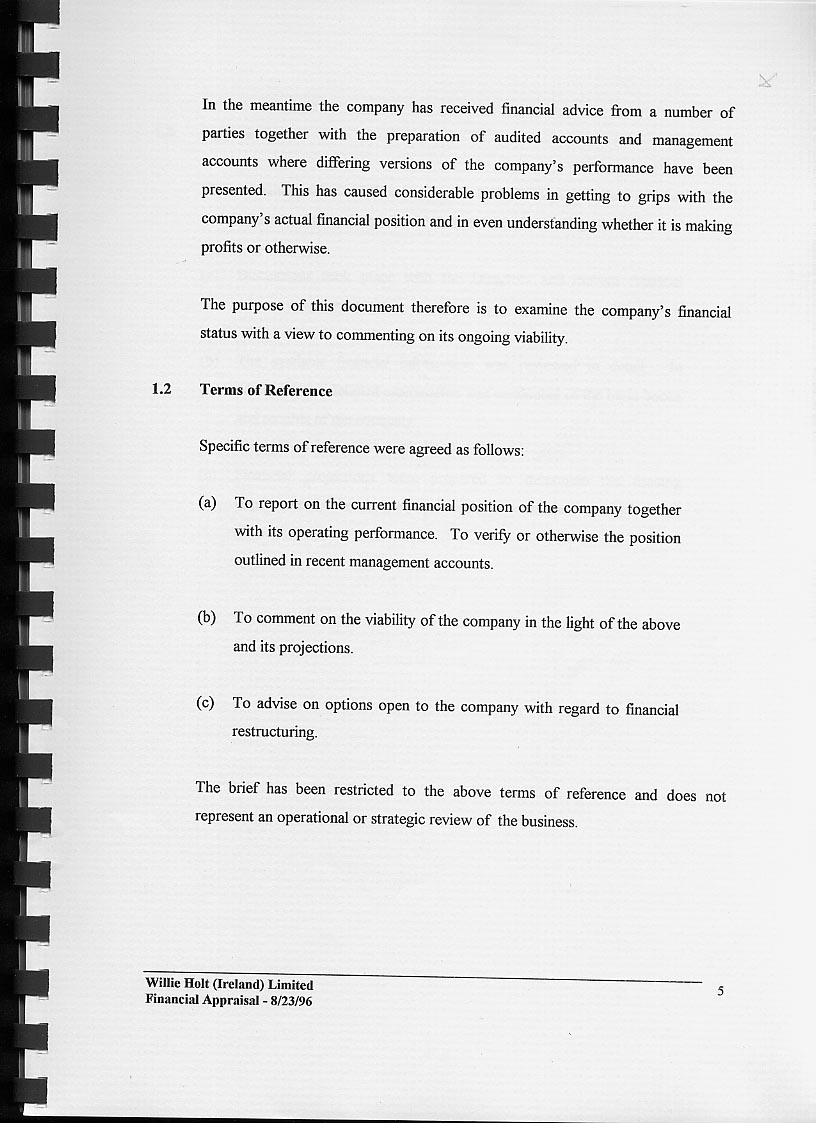

So on the 13th of August Martin Cole comes to the factory for 4 days to check the accounts. The other days would be required I assume to type up his report. I can assure the reader there was no “Management Development course”. Eventually Mr. Cole’s report arrived and concluded that Mr. Sheehan’s figures were more or less correct::

|

|

While we were pleased with confirmation of our profits we found the rest of the report an outrageous misrepresentation.

|

|

On page 4 of the report Mr. Cole indicates that Gauselmann have stopped prepayments on tables. The position was that Gauselmann would prepay as long as required and it had always been assumed that we would go over to payment on delivery when the IDA incentive of the building was realized. There was never a suggestion that Gauselmann would pull the plug. This was not in their interest. This was not true and would only be true in the case where we lost control of the company. This statement represents a gross misrepresentation. In fact Gauselmann continued to pay in advance until we were allowed to escaped from the trap our project had become more than a year later.

He also states that we "had sought Forbairt Support.” This is totally untrue. The only thing we wanted from that organization was to see the back of them.

The only thing we required, and indeed the only thing that the project required, was that what we were told before we came to Ireland or as a compromise what we were told after we came to Ireland be the truth. That is All.

Did not Mr. Cole also received his paperwork from FAS? The contrast between Mr. Cole's terms of reference and the FAS terms of reference is remarkable.

There were two possible options and this was made very clear to Mr. Cole.

- Option A. IDA keeps its word and we live in Ireland as a family and the project continues in Ireland and this option needed to be financially modeled.

- Option B. IDA does not keep its word and we depart and this option needed to be financially modeled.

Mr. Cole has decided not to model either option A or B. Instead he is in fact modeling IDA/Forbairt’s preferred option whereby we would not get the building and I would remain entrapped in Ireland with my children in another country. If we are being used as a means to embezzle EU funds then this also would mean that IDA/Forbairt can keep their “nice little earner.”

Given that we are talking about a financial appraisal and not an Audit items that will have a bearing on the alternative deals that could be put together but which would not normally appear in a formal balance sheet are of vital significance. Two very important items to consider were:

- How much was the company worth.

- How much did we have to pay IDA if we sold to a competitor.

Mr. Cole puts a value on the Designs and Brand of IRP 43k which is a laughable amount when one considers:

- that this was an internationally recognized and respected brand

- the fact that the Mantis table had been awarded Germany’s highest industrial design prize

- the amount spent buying the brand and developing new products

- the amount that had been recently spent (25k) on new catalogues and corporate image

- the fact that the amount being spent promoting the brand only in Germany in a single year was more than 43k.

- the proven level of orders that the brand and designs were capable of generating

We believe that Forbairt now had what they needed. They adopted a “fire sale” balance sheet definition of insolvency. This was facilitated by valuing this profitable company with an internationally recognized brand, a three million DMark order book, award winning designs, together with plant machinery and goodwill at a pittance and by accepting that we had no rights under the incentive package which brought us to Ireland.

Obviously a company is deemed to be insolvent if it has either ceased to pay his debts in the ordinary course of business or cannot pay his debts as they become due and this was clearly not the case. For details on this “Solvency issue” click here

|

The fact that the sale of the building to the company on the terms agreed with IDA before the company relocated to Ireland would solve the entire problem is understated to say the least. In fact initially Mr. Cole was not going to mention this at all and only included some brief mentions after considerable pressure from me. |

|

|

Mr. Sherry did not read large parts of the report in any case. Confirmation of this fact in this sound bite. Obviously he did not feel it worth his valuable time. Indeed over the coming nine months during which I was forced to kowtow to this individual he never once took the time to visit the factory. |

"Thats not how I read it"! |

A Page He Did Not Read. |

Another Page He Did Not Read. |

In fact the report accepts without question that the company has no right to buy the building for less than value. This report then describes the consequences of this huge financial “disappearance” and compounds the resulting “crises” by suggesting that Gauselmann would change our terms of trade removing another 85k from cash flow.

It is worth noting that the value of a manufacturing business is usually taken at 8 to 10 times its profitability. This would value Holts at this point at between IRP 640,000 and IRP 800,000. The Irish State agencies would over the coming 18 months completely destroy this value. By leaving us in a situation of total uncertainty they destroyed our ability to realize the true value of this business. In our opinion this was intentional as they wanted to keep us in Ireland in a sort of indenture. So what was the motivation? Were they milking the EU system. Were these agencies acting in support of a criminal fraud?

Was this the only time that Mr. Cole or his clients received EU funds thanks to Mr. Sherry?

Please take the time to answer our Poll on the right hand side of this page and if you have any comments use the “comments” link at the bottom of this page.

User login

Navigation

Add Your Story

If you have had an experience in dealing with the Irish state agencies and you feel that your story would be helpful to companies coming to Ireland please use the link provided on this page to begin the process of adding your story to this website.

{kind=link}